Featured

Table of Contents

Clients that enroll in the AMP program are not qualified for time payment plan. Web Power Metering (NEM), Direct Accessibility (DA), and master metered customers are not presently qualified. For customers intending on relocating within the following 60 days, please apply to AMP after you've established service at your new move-in address.

One essential element of debt forgiveness relates to tax standing. The basic rule for the Internal revenue service is that forgiven debt income is taxed.

The PSLF program is for borrowers that are employed full-time in qualifying public service work. You would have to be qualified when you have made 120 qualifying settlements under a qualifying repayment plan while benefiting a qualifying employer. Once you have actually fulfilled this demand, the balance on your Direct Car loans is forgiven.

Initial Consultation and What to Expect Can Be Fun For Everyone

This is to motivate instructors to serve in locations where they are most needed. IDR plans to readjust your month-to-month trainee financing settlement amount based on income and family dimension. Any type of exceptional equilibrium is forgiven after 20 or 25 years of qualified payments, depending on the certain selected real plan.

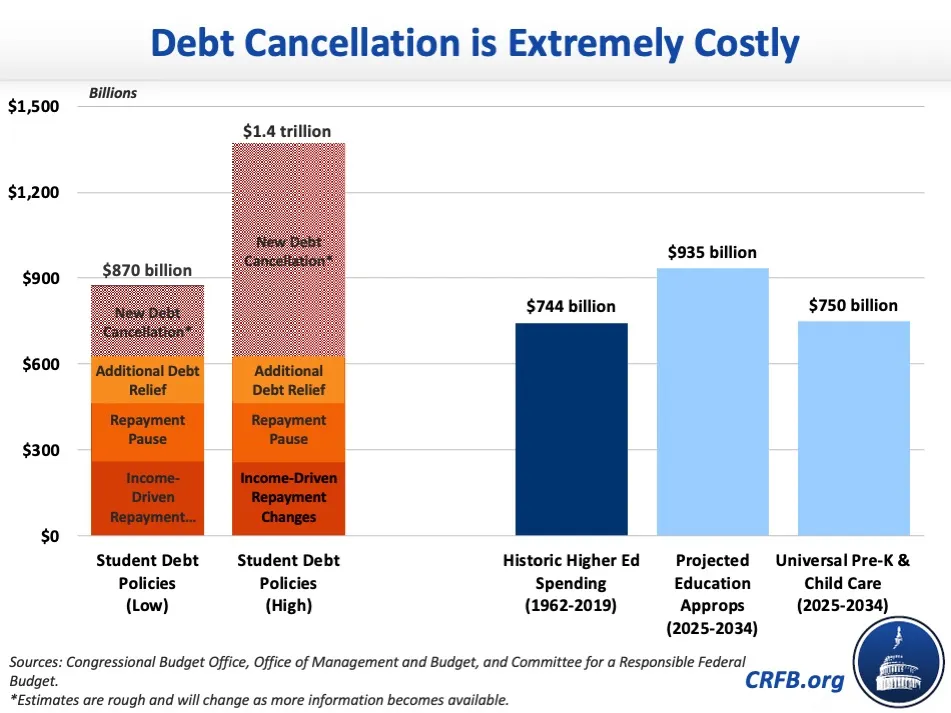

The CARES Act put on hold funding settlements and established interest prices at 0% for qualified federal pupil car loans. Private student lendings can not be forgiven under the government financing mercy programs since they are released by exclusive loan providers and do not carry the backing of the federal government.

Refinancing: Occasionally, a consumer obtains a new loan with far better terms to settle existing car loans. Paying off may entail a reduced rate of interest or more workable month-to-month repayments. Combination: combines numerous lendings into one, making the payment less complex. Good credit scores is required, so not all consumers might certify.

The Main Principles Of Restoring Your Credit History Post Best Repayment and Forgiveness Programs for Medical Professionals

Some exclusive loan providers use case-by-case challenge programs. These include briefly making interest-only settlements, temporarily reducing payments below the contract price, and even various other forms of lodgings. Borrow against those possessions, like cash value from a life insurance policy policy, or take car loans from family members and close friends. Such alleviation is, however, temporary in nature and features its own collection of risks that have to be carefully weighed.

Some of the financial obligations forgiven, specifically originated from debt settlement, likewise negatively influence credit score scores. Doubters say forgiveness programs produce a setting for careless loaning and established false expectations for future bailouts. Often, the argument regarding debt mercy concentrates on its long-term results. Some argue that widespread debt mercy will produce a criterion for obtaining an increasing number of without paying back the quantities, anticipating mercy in the future.

Forgiveness of large quantities of debt can have substantial monetary implications. It can contribute to the national debt or necessitate reallocation of funds from other programs. Policymakers, as a result, have to balance the instant direct advantages to some individuals with the general economic impact. There are disagreements that financial debt mercy is not fair to those that already settled their finances or followed less costly courses of education.

Understand that your car loans might be purely federal, purely personal, or a combination of both, and this will factor right into your choices. Forgiveness or repayment programs can conveniently line up with your long-lasting financial goals, whether you're buying a house or preparation for retired life. Be aware of exactly how the different kinds of financial debt alleviation may affect your credit report and, later on, future loaning capability.

An Unbiased View of Financial Impact the Expense of Bankruptcy Counseling

Financial obligation mercy programs can be an actual lifesaver, yet they're not the only means to tackle placing financial obligation. They can reduce your month-to-month payments now and may forgive your continuing to be financial obligation later on.

2 ways to pay off financial debt are the Snowball and Avalanche approaches. Both aid you concentrate on one debt at a time: Pay off your tiniest financial obligations.

Prior to deciding, think concerning your very own cash situation and future plans. It's wise to discover all your choices and talk with a money specialist. In this manner, you can make choices that will certainly help your financial resources in the lengthy run. Internal Profits Solution. (2022 ). Canceled Financial Obligations, Repossessions, Repossessions, and Desertions (for People).

Unlike financial obligation consolidation, which combines multiple financial debts into a solitary finance, or a financial obligation administration strategy, which restructures your repayment terms, financial obligation forgiveness straight minimizes the principal balance owed. The staying balance is then forgiven. You may select to work out a negotiation on your own or get the help of a financial debt settlement business or a skilled financial obligation assistance attorney.

Not just anyone can obtain charge card debt forgiveness. You normally require to be in alarming monetary straits for lending institutions to even consider it. Particularly, creditors check out different elements when considering debt forgiveness, including your revenue, possessions, various other financial obligations, capacity to pay, and readiness to cooperate.

10 Simple Techniques For How APFSC Ensures Legal Compliance

In many cases, you may have the ability to solve your financial obligation situation without turning to insolvency. Prioritize essential expenditures to improve your economic situation and make area for financial obligation settlements. As an example, try to find methods to reduce discretionary expenses, such as streaming registrations and eating in restaurants. If you can not solve your financial obligation problems in various other methods, reach out to your charge card issuers to discuss your economic difficulty.

{kind=link}

Table of Contents

Latest Posts

Some Known Details About Developing a Personalized Route to Relief

How How to Not Repeat the Previous Patterns After Debt Relief can Save You Time, Stress, and Money.

The 30-Second Trick For Free Educational Financial Literacy Workshops Offered by APFSC

More

Latest Posts

Some Known Details About Developing a Personalized Route to Relief

How How to Not Repeat the Previous Patterns After Debt Relief can Save You Time, Stress, and Money.

The 30-Second Trick For Free Educational Financial Literacy Workshops Offered by APFSC